A History of Blood – Vol. 2, Chapter 12

The last two chapters I’ve talked about the products I sell, Life Insurance and Annuities. This chapter will be a bit more about the sales process and one of the most important documents to review with a potential agent or client: the Financial Life Strategy, also known as a fact-finding.

The Financial Life Strategy (FLS) is a document unique to PHP Agency, but the concept of fact-finding interview (sometimes called a needs-analysis) is an industry standard. This document is the bridge between a business prospect and a new client, and it sets the stage for a successful agent-client relationship, by introducing some of the core concepts that different insurance products address.

The first thing to understand is that all the numbers included on illustrations are for educational purposes, with some aspects being guaranteed, and other aspects being based upon current interest rates or current inflation rates, depending upon the type of product being sold.

Life Insurance is a phenomenal estate strategy. By providing a tax-free death benefit upon the death of the insured, an estate is instantly created. It’s worth noting that in order to get the death benefit tax-free, there must be a named beneficiary. The most common beneficiaries are a surviving spouse, an adult child, or a charity such as a church or temple. It’s also worth noting that a policy can have more than one beneficiary, granting either a percentage or a fixed amount whom whoever the policyholder chooses.

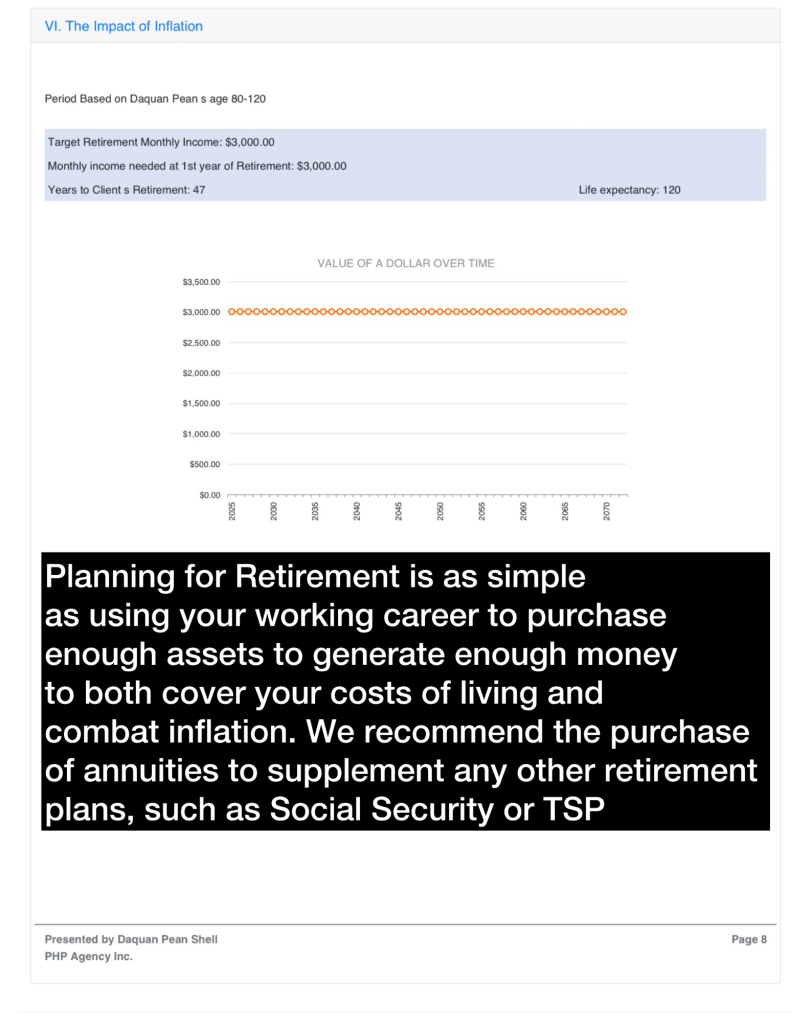

Annuities, by comparison, are incredibly powerful retirement strategies. They provide guaranteed income streams without any additional effort. The most important part of an annuity is making sure the final payment amount is enough to make a meaningful difference in the policyholder’s lifestyle. As we’ve reviewed in the previous chapter, a $1M annuity typically results in an income of between $5,000 and $10,000 per month.

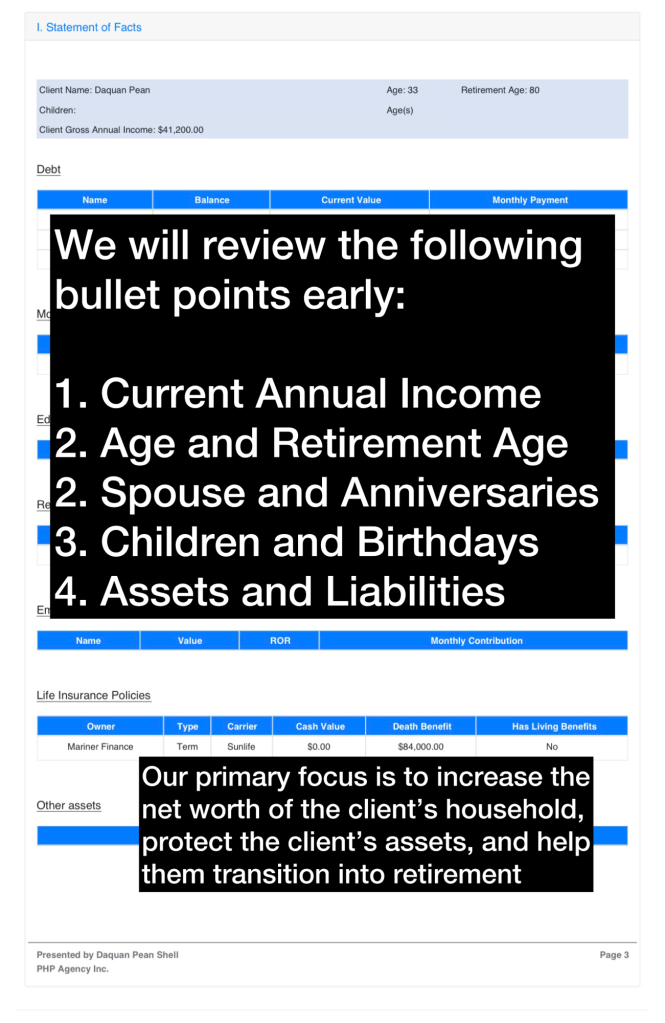

The first steps to review when completing the FLS are the clients annual income, their spouses annual income, their ages, and their desired retirement ages.

The average working career lasts 35 years, with the full retirement age being 70, and early retirement being possible as early as 62.

The average person changes employers every 4 years (or less) and one of the benefits of an annuity is that you take it with you as you change employers, also taking your life insurance with you as well.

The average life expectancy is about 80 years old, meaning that, generally speaking, you should be planning live off of your working wages for the first 35 years of your career, afterwards, you have the option of “cashing out” or continuing to work while still receiving the additional retirement income.

For example, a 70 year old man could potentially receive wages from his job, income from social security, and income from annuity, with the social security and annuity paying out until he dies, and then receiving a lump sum through life insurance at the time of their death. It’s worth noting that the current president of the United States is 79 years old and still going strong.

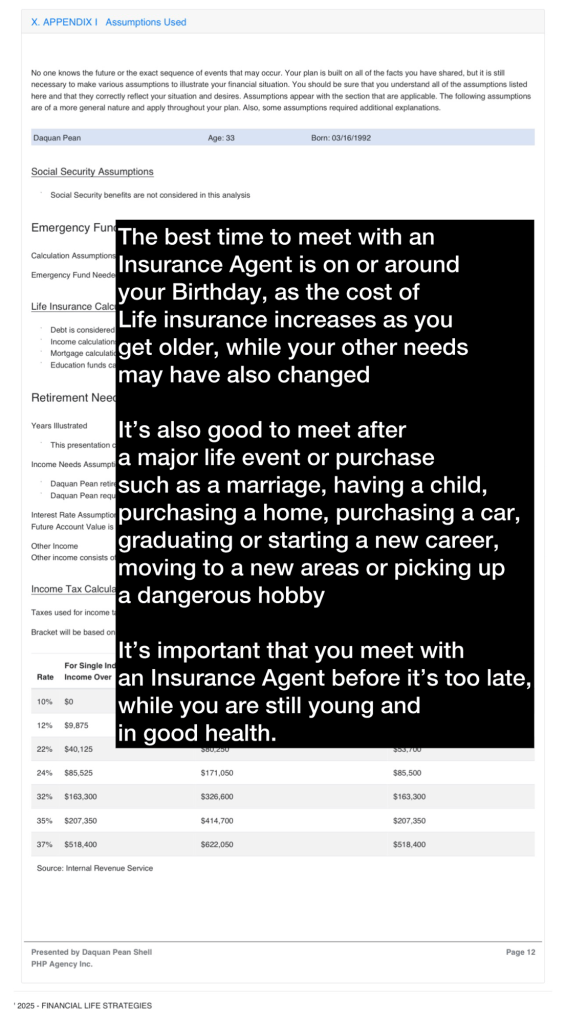

While the above section focuses primarily on age and retirement age, it also includes important dates such as your wedding anniversary, your wife’s birthday, and your children’s birthday. It’s worth noting that the cost of life insurance is based on age, so every year the products get more expensive, with how much more expensive being based upon the proposed insured life and lifestyle.

Outside of that, this section also includes key information about the families finances, such as income, assets, and debts. As a person progresses through their career, and their relationship with their agent develops, they should both make it a good to get higher incomes, net worths, more children and longer marriages.

For the most part, life insurance has four major uses:

- Final Expenses: used to cover the costs of burial, funeral services, and any remaining debts or legal fees

- Income Replacement: used to replace the income of a breadwinner

- Mortgage Protection: used to cover the remaining mortgage or pay for housing expenses

- Education: used to make private education or higher education more affordable for survivors.

Balancing or prioritizing these needs is all are a part of the job of an agent.

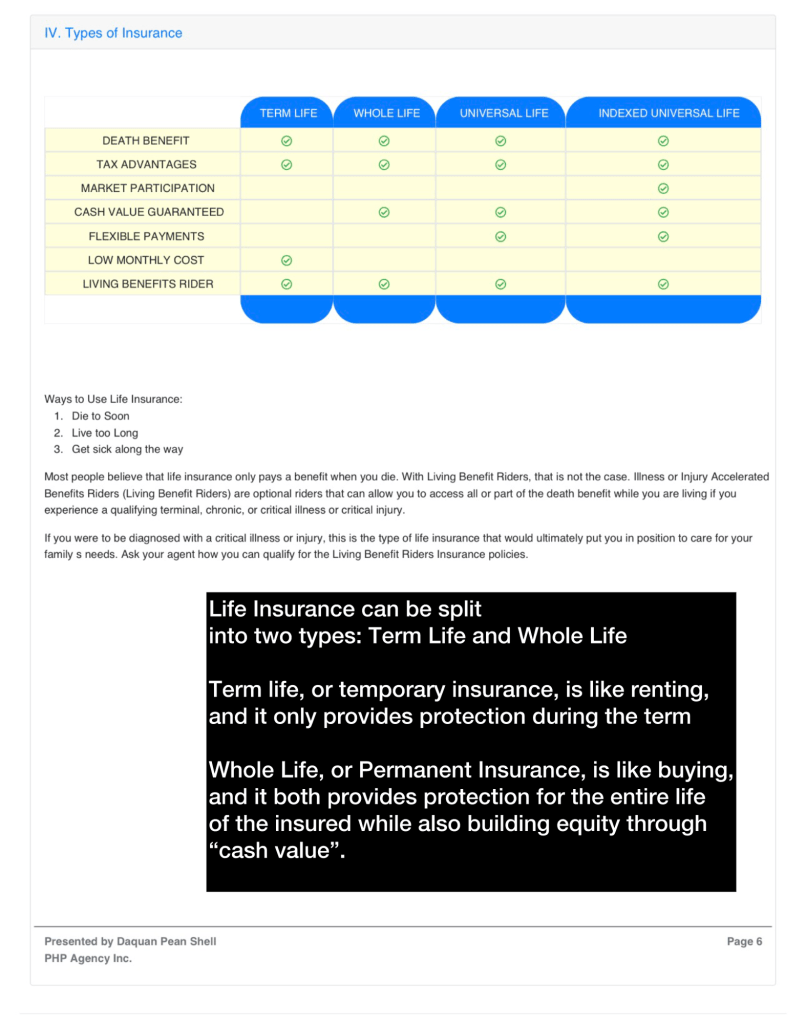

Life Insurance comes in two forms: term life (or temporary life insurance) and whole life (permanent life insurance).

Both types offer a tax-free lump sum at the death of the insured, but they are different in the way they go about it.

Term life is the more affordable option, offer a higher face values for lower premiums. The downside is that is the proposed insured survives the term, they get nothing, and while they can sometimes renew at a higher rate, it’s possible they are no longer insurable if their health has deteriorated too rapidly.

Whole life is the more expense option, but offers significantly more comprehensive protection. While the downside is a lower face value and a higher premium, the insured is both guaranteed to receive the death benefit and guaranteed to build cash value over the life of the contract. Some contracts even come with a dividend option, allowing the policyholder to either create an additional income stream, or purchase additional insurance at no additional cost. Once a whole life insurance is in force, no additional insurability is required.

While it typically takes 2-3 years for a policy to start accruing cash value, the cash value allows the policyholder to take a policy loan based on that value, with the loan being low-interest, and the income being considered tax-free.

Considering you can also purchase life insurance with pre-tax dollars, there is a larger tax advantage to whole life (and universal life) when compared to term life. It’s worth noting you can also purchase annuities with pre-tax dollars, assuming the annuity is qualified, but if the annuity is qualified there will be contribution limits.

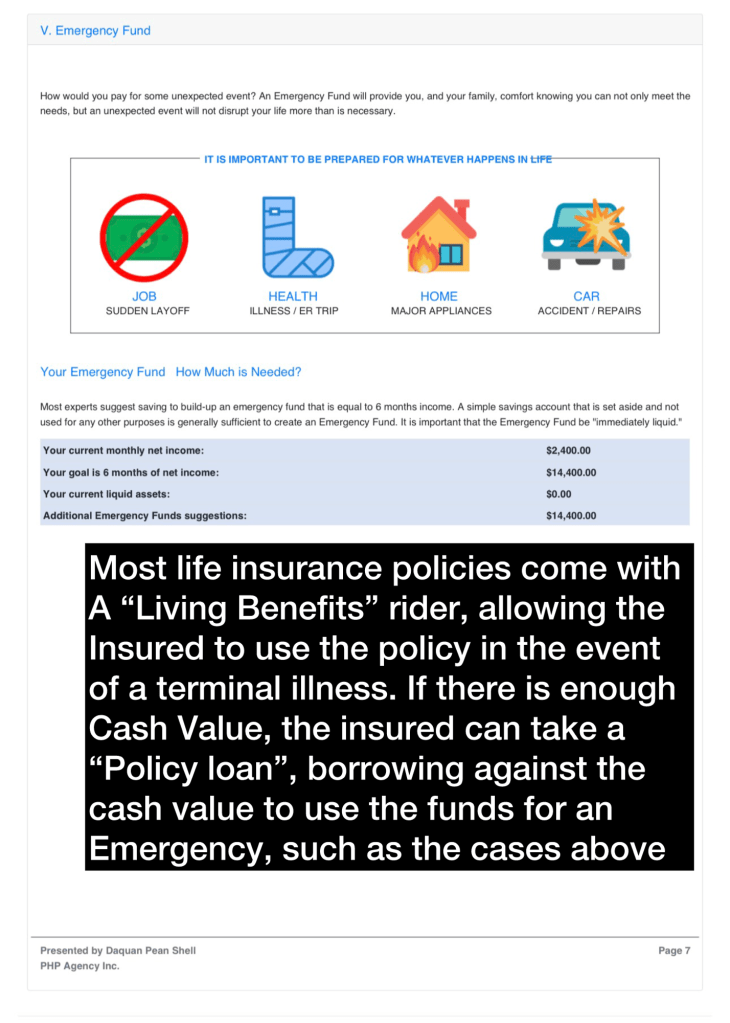

6 months of living expenses is not just great general financial advice, it’s also essential for those considering starting a business or otherwise switching to a commission only compensation plan as opposed to a regular salary.

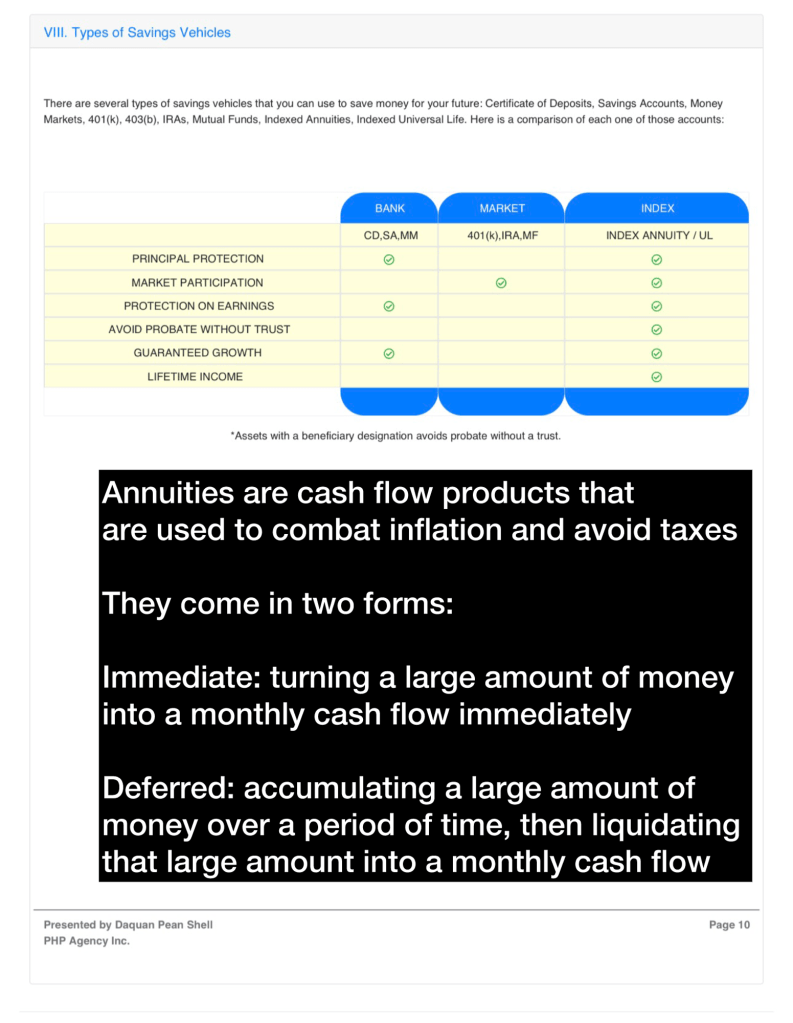

The target monthly retirement is typically made up of Social Security (assuming the policyholder plays taxes) and various annuities if the client is self-employed. Buying multiple annuities allows the client to both diversify with annuities that offer deferred payments in some cases and more immediate payments in others.

It’s worth noting that larger initial deposits typically offer higher interest rates than deposits over time.

Generally, the rates vary between 4% and 8%

When I worked as a moneylender in early 2025, I did about 400 or so fact-findings for different clients, with about half of them working and the other half retired. While there were plenty of retirees that had multiple streams of income, there were some that only received Social Security.

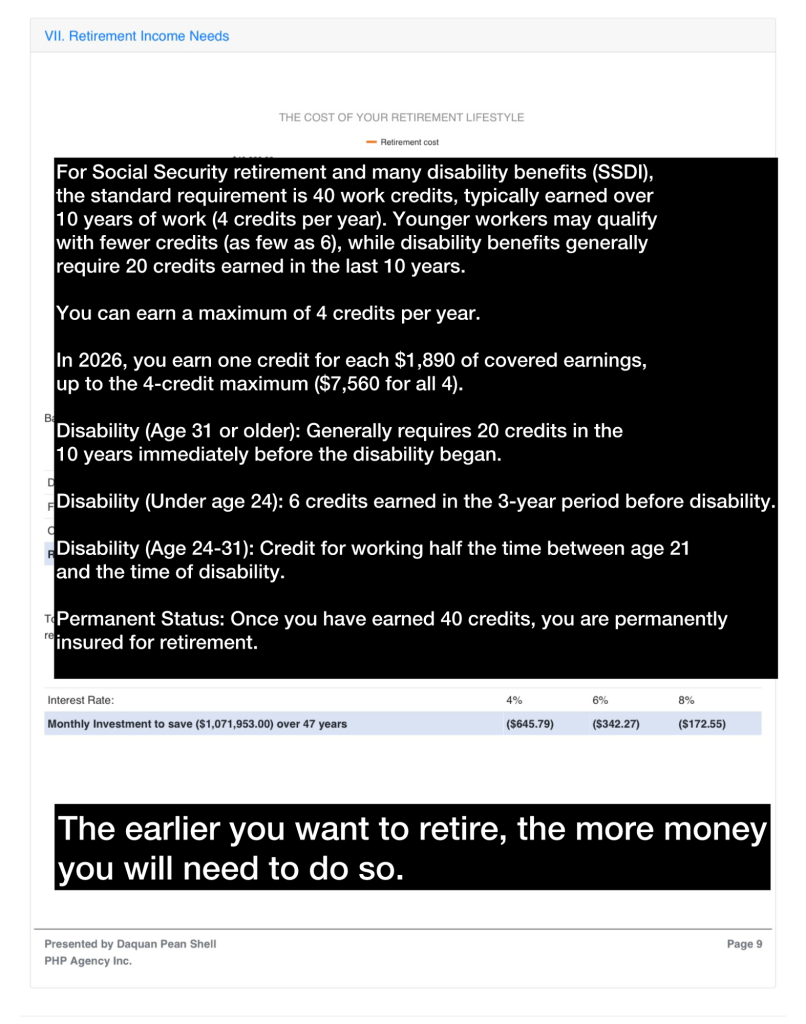

The way Social Security works is simple: you pay into it over your working career, and once you start retire, you receive a monthly income based upon your 35 highest earning years, with the monthly income also being adjusted for inflation. The minimum amount of years required to qualify for Social Security is 10. You can earn a maximum of 4 credits per year, and it requires a minimum of 40 credits to qualify.

Once you qualify for Social Security, you are permanently insured for retirement.

Generally, annuities come in two forms: immediate and deferred. An immediate annuity is typically purchased using a lump sum of money, resulting in a lifelong income stream, while a deferred annuity is typically funded over time, yet achieving the same result in the end. While not always the case, immediately annuities tend to have better interest rates than their deferred counterparts.

Annuities can also be “qualified” or “non-qualified”.

A qualified annuity is funded with pre-tax earnings, allowing the growth to be tax-deferred, but is subject to contribution limits (typically $10,000). The entire withdrawal is taxed as regular income.

A non-qualified annuity is funded with after-tax earnings, and the growth is also tax-deferred but there are no contribution limits. While the principal is returned tax-free, the earnings (or gain) is taxed as ordinary income.

Assuming the agent is licensed, the fact-finding is immediately followed by the presentation of a combination of life insurance and annuities.

Some slogans:

“life insurance in case you die, and an annuity in case you don’t”.

“Life insurance is the jab but the annuity is the cross”

“The annuity is the thunder, life insurance is the lightning”

Some insurance polices require medical exams.

Typically, term insurance requires a medical exam if the face value is above a certain amount, while whole life insurance can have the option of a medical exam in exchange for a lower premium. If the policy does not require a medical exam, all it needs are signed illustrations, a completed application and submitted premium to be considered in force. If the policy does require a medical exam, however, it will not be considered in force until after the exam is completed, and the above three criteria are met.

It’s important to meet with your insurance agent regularly, as our income, career, and insurance needs and options change over time. The same way you meet your doctor once a year for an annual checkup, you should meet your agent once (or twice) a year for an annual review of your finances.

While each situation is different, here are three basic goals that should apply to every situation:

- Enough life insurance to cover final expenses ($15K~ per person) whole or term

- Earned $1M over the course of working career ($30K per year)

- Minimum of $150,000 account value (annuities) prior to retirement.

As of early 2026, the average annual salary for an insurance agent in the United States is approximately $60,000–$71,000, with most earning between $49,000 and $75,000.

While starting salaries often fall around $32,000–$40,000, experienced agents, particularly in specialized fields or high-cost areas, can earn well over $100,000 annually.

Top 90th percentile earners often make over $98,000-$120,000 annually.

Salary heavily depends on experience, licensure, location, and whether the agent is captive (salary + commission) or independent (commission-heavy).

Most agents receive a base salary plus commission, while others work on a commission-only basis, allowing for high income potential but higher risk.

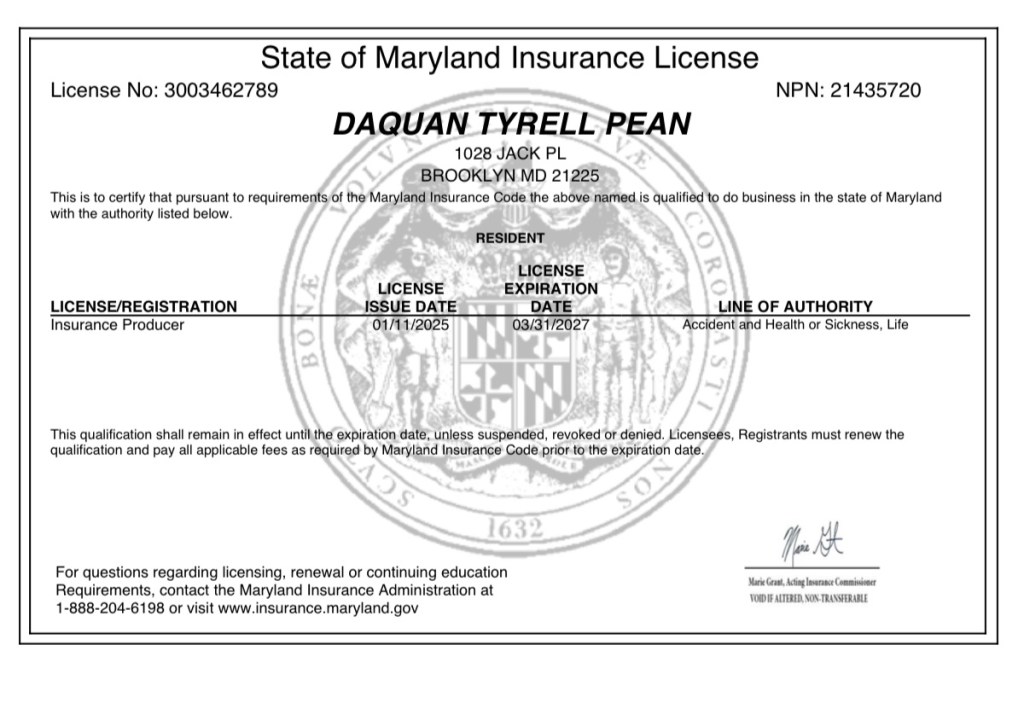

I became an insurance agent on April 16, 2018 — but I didn’t actually get licensed until January 11, 2025, a little over a year ago.

Over the course of my working career as a whole, I’ve made $271,563, or $24,687 per year over 11 years, spending most of that time unlicensed.

I made $29,656 in my first year as a licensed agent, but I didn’t actually work from September to the end of the year, mourning the loss of my friend and business partner, Jaime Allison Morgan.

The day before Jaime died, I asked my current wife to marry me.

She said no at first, but after I told her I was going to marry someone else she changed her mind. We had sex again but I wasn’t actually satisfied.

I told her I wanted a real, legal marriage with a marriage license similar to my insurance one, but she claimed “she didn’t know her social”. About a week later she got arrested and got a DUI. It is what it is.

I love my wife dearly but holy moly.

Part of the reason I fell in love with her was the timing that I met her. I met her when I was struggling with alcoholism myself, at a time before I was a veteran, before I was an insurance agent, before I was a Priest, before I was anything significant. She is my Proverbs Chapter 8:

Leave a comment